PROJECT TYPE

B2B Fintech · Feature Design · Desktop & Mobile

CLIENT

Shift

MY ROLE

Lead Product Designer

TIMELINE

3 months (Jan 2023 - Mar 2023)

OVERVIEW

Shift provides financing solutions that allow businesses to access working capital through credit lines. However, increasing credit limits was a manual, time-consuming process that relied heavily on the support team.

I led the design of a self-serve credit limit increase (CLI) experience, enabling businesses to request and receive additional credit directly within the platform. This feature reduced operational friction while helping the business achieve its goal of increasing the amount of capital deployed to customers.

MY RESPONSIBILITIES

Creative Direction, Visual Design, Design Language, UX, Interaction Design

IMPACT

Turning the experience around

The feature delivered measurable business impact within 90 days.

$2M

Increase in business credit issued in the first 3 months

0 days

Approval time for pre-approved businesses on the instant path

-22%

Reduction in support calls related to credit limit requests

THE PROBLEM

Businesses were hitting their credit ceiling with no way to act on their own

Increasing a credit limit required calling support, being transferred to the credit team, answering questions, and waiting several days for a decision. Customers had no visibility into the process, and the support team was fielding a volume of requests that could have been handled online.

The goal was to bring this into the platform, removing the dependency on the phone queue, enabling instant approvals where the data already supported them, and keeping the right controls in place for cases that required manual review.

"This creates a bottleneck in credit growth, directly limiting the amount of funds Shift can deploy."

- Head of Product, Shift Credit Platform

RESEARCH

The existing experience

- Customer contacts Shift support

- Support transfers request to the credit department

- Customer answers a series of credit questions

- Documentation may be requested

- Approval can take several days

Customer pain points:

- Slow and inconvenient

- Lack of transparency on application status

- Multiple touchpoints required

RESEARCH

The business impact

- Support team overloaded with manual requests

- Credit team processing applications inefficiently

- Friction preventing customers from accessing additional credit

This created a bottleneck in credit growth, directly limiting the amount of funds Shift could deploy.

BUSINESS GOALS

Design a self-serve credit limit increase feature that:

- Eliminates the need to call support

- Provides a clear and transparent application process

- Enables instant approvals where possible

- Maintains compliance with credit and risk policies

- Ultimately increases the amount of capital deployed

"The problem isn't just the lack of a self-serve feature, it's the complexity of the credit decision process behind the scenes."

- CRO, Shift Credit Platform

DISCOVERY

Understanding the problem before designing the solution

To understand how automation could work safely, I collaborated closely with the credit, risk, and support teams before any design decisions were made.

The key questions driving the research were straightforward: what data was needed to approve a credit increase, which criteria could support an instant decision, which cases genuinely required manual review, and what regulatory requirements couldn't be moved. Getting clear answers to all four was a prerequisite for designing anything.

KEY FINDINGS

Many businesses could safely receive instant credit increases based on existing data.

- Existing repayment history

- Credit risk rating

- Security already held by Shift

- Current utilisation and financial profile

KEY FINDINGS

More complex requests would still require manual review by the credit team.

Mapping the current process alongside real customer scenarios made it clear that the opportunity wasn't just to digitise the phone workflow - we could separate instant approvals from manual reviews, allowing the platform to handle straightforward cases automatically.

CONSTRAINTS

Three factors shaped what the solution could and couldn't do

Designing within this space meant working around fixed requirements from three distinct teams, each with rules that couldn't be removed or simplified, only designed around.

Compliance owned what data had to be collected and when. Engineering was responsible for systems that didn't talk to each other. Risk set the sign-off rules that governed every credit agreement.

Getting the feature to work meant all three were embedded in the process from the start.

Compliance

Data collection, document requirements, and sign-off rules were fixed. Compliance reviewed every decisioning rule.

Engineering

Eligibility checks, automated decisioning, and FLA generation ran on separate, unconnected systems.

Risk

Any FLA required digital signatures from all directors. This couldn't be bypassed, even for pre-approved customers.

How can we enable businesses to access more credit without picking up the phone, while giving the credit team the controls it needs to manage risk responsibly?

RESEARCH

Affinity mapping

Through a series of workshops with the credit, risk, and support teams, we mapped how credit limit increases were currently handled and identified where the process broke down. Insights from each team were grouped by theme; what triggered a request, what information was needed to make a decision, where handoffs caused delays, and what data already existed in the platform.

Surfacing these patterns across teams helped build a shared understanding of the problem before any design decisions were made.

RESEARCH

Surfacing opportunities

Mapping the existing process made it clear that the bottleneck wasn't caused by a single point of failure, it was structural. Every request followed the same manual route regardless of complexity.

The opportunity was to let the data do the work: businesses with strong repayment histories and sufficient security didn't need a phone call.

Separating those cases from more complex ones meant the platform could deliver a meaningfully different experience for each, without compromising risk controls for either.

RESEARCH

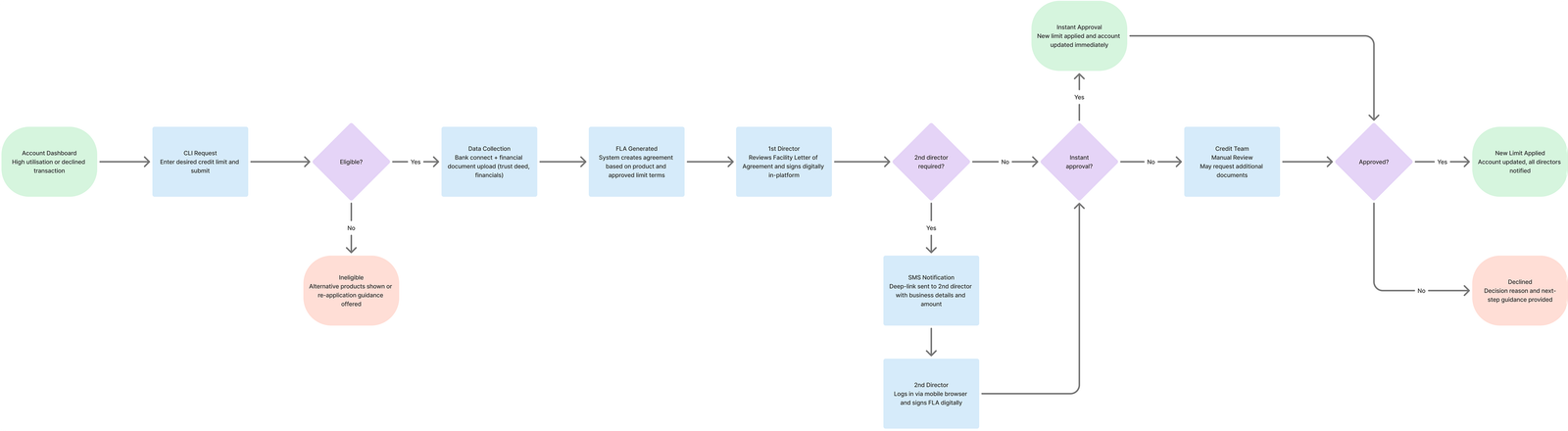

Mapping the full lifecycle

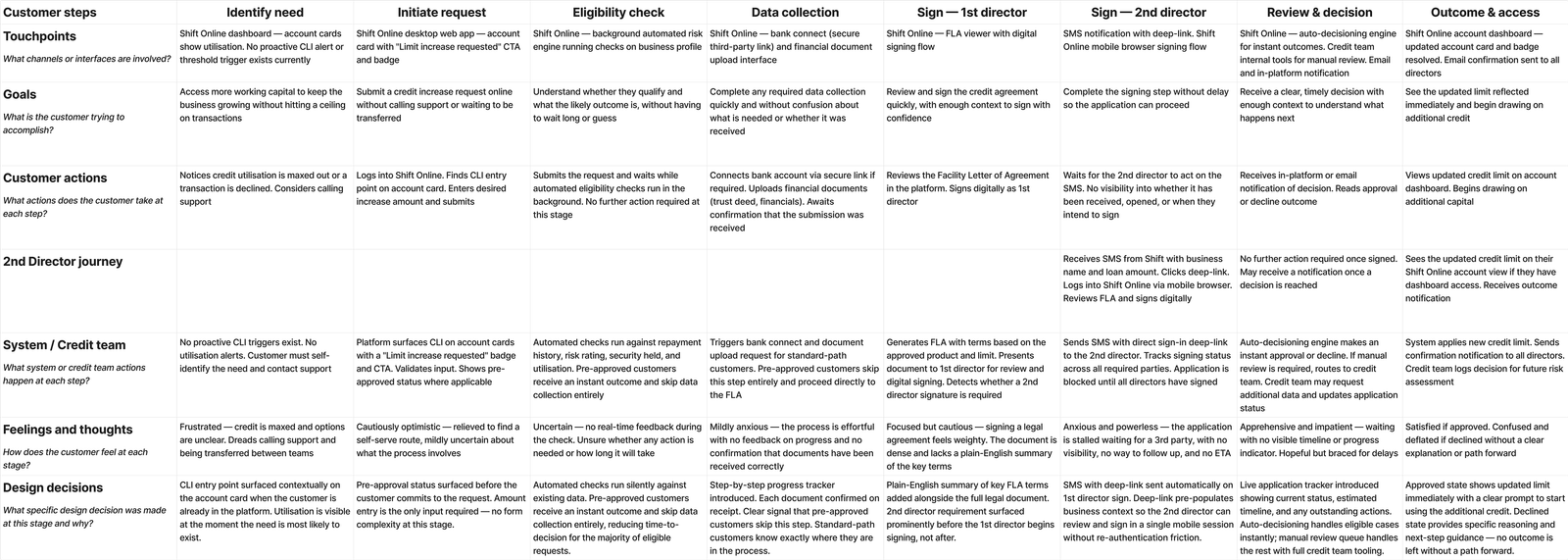

The journey map was structured across multiple lanes - customer (1st director), 2nd director, system and credit team, and touchpoints. Mapping these together helped the team understand not just the user experience but the internal decision points required to approve credit safely.

The journey covered nine distinct steps: from identifying the need and initiating a request, through eligibility checking, data collection, FLA signing across both directors, credit decisioning, and final outcome. By mapping interactions across teams, it became easier to identify where automation could happen safely and where human review was still required.

The existing CEJ with pain points and opportunities.

DESIGN

Balancing speed with risk and compliance requirements

When designing the feature, the main challenge was balancing two competing needs:

- Speed for customers who needed access to more credit quickly

- Risk and compliance requirements from the credit and finance teams

Through discussions with the credit team, it became clear that not every request needed the same level of review. Some businesses already had strong repayment histories and sufficient security in place, meaning their credit limits could safely be increased without manual assessment. Others still required a more traditional review process. To support both cases, the solution was designed around two clear paths: an instant approval route for businesses that met predefined credit criteria, and a structured manual review route for those that required deeper assessment.

DESIGN

The two-path decision architecture

Instant approval for eligible businesses, manual review for complex cases.

DESIGN

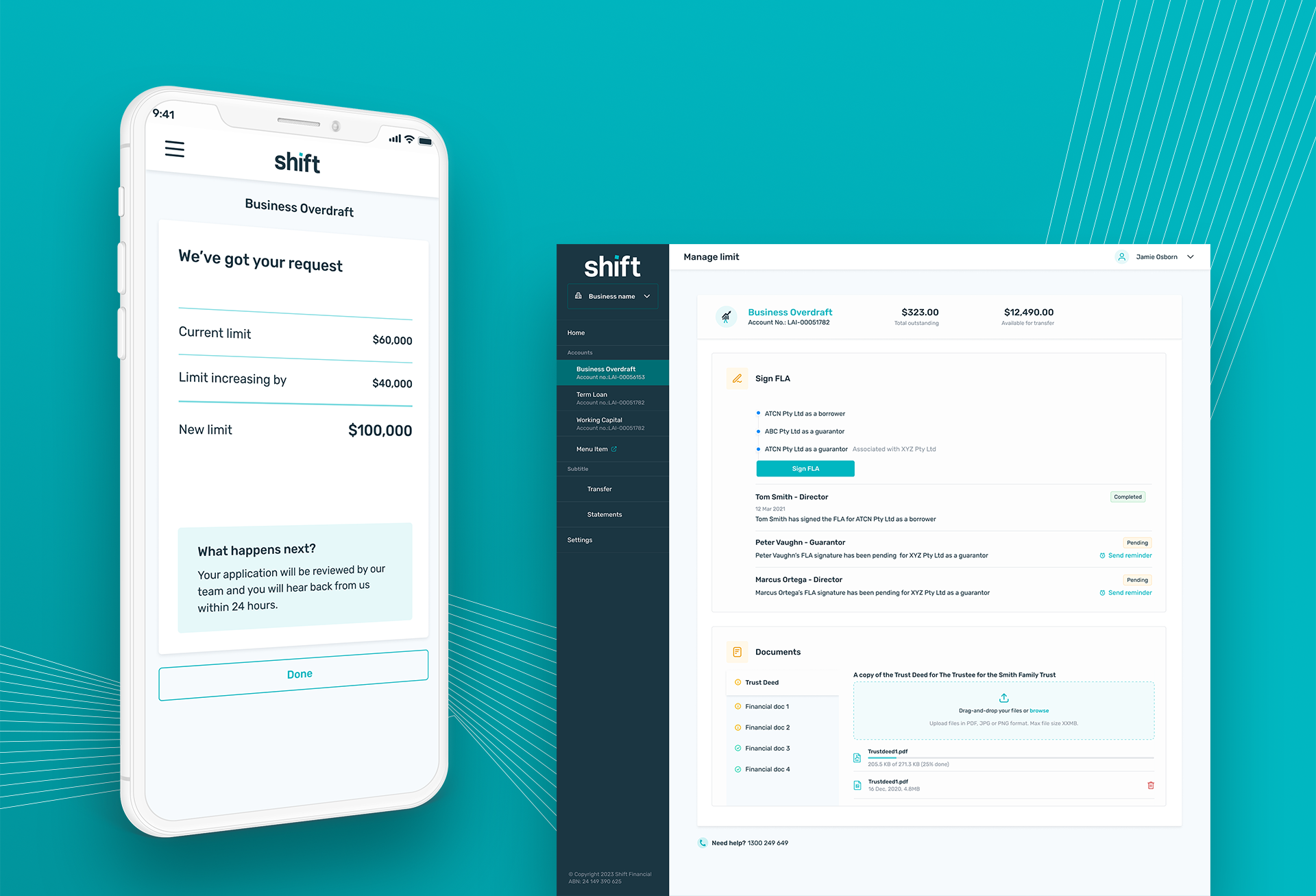

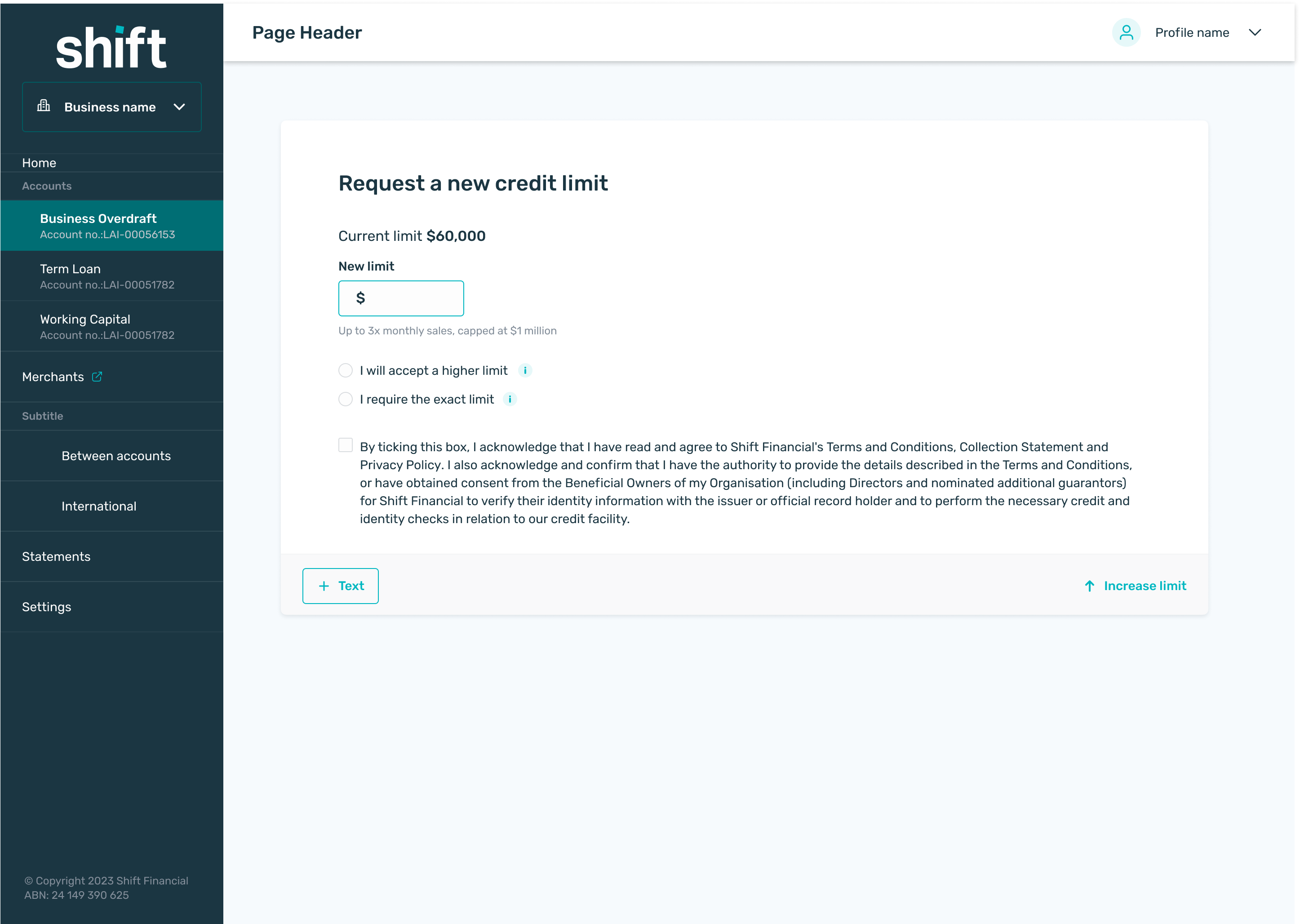

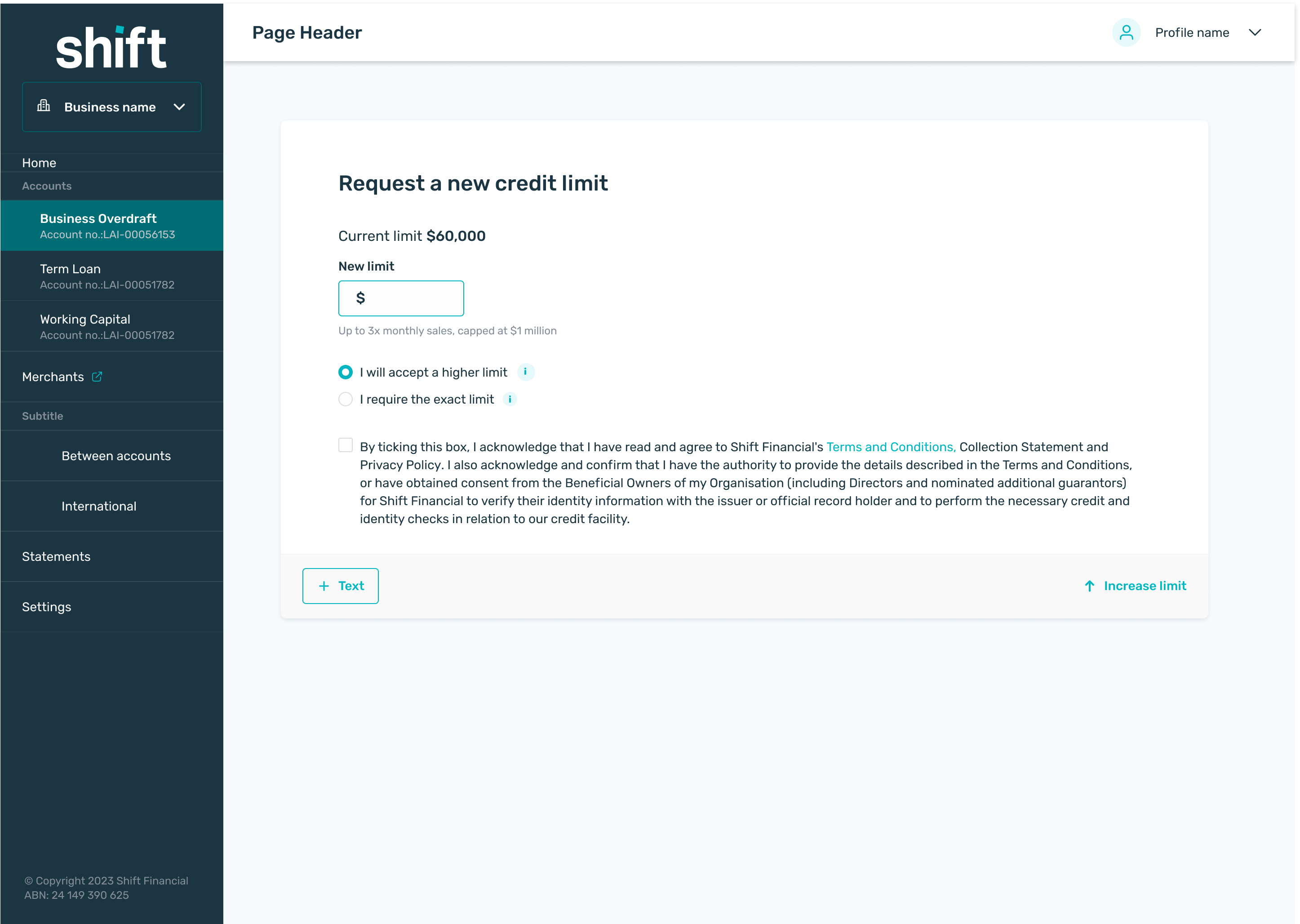

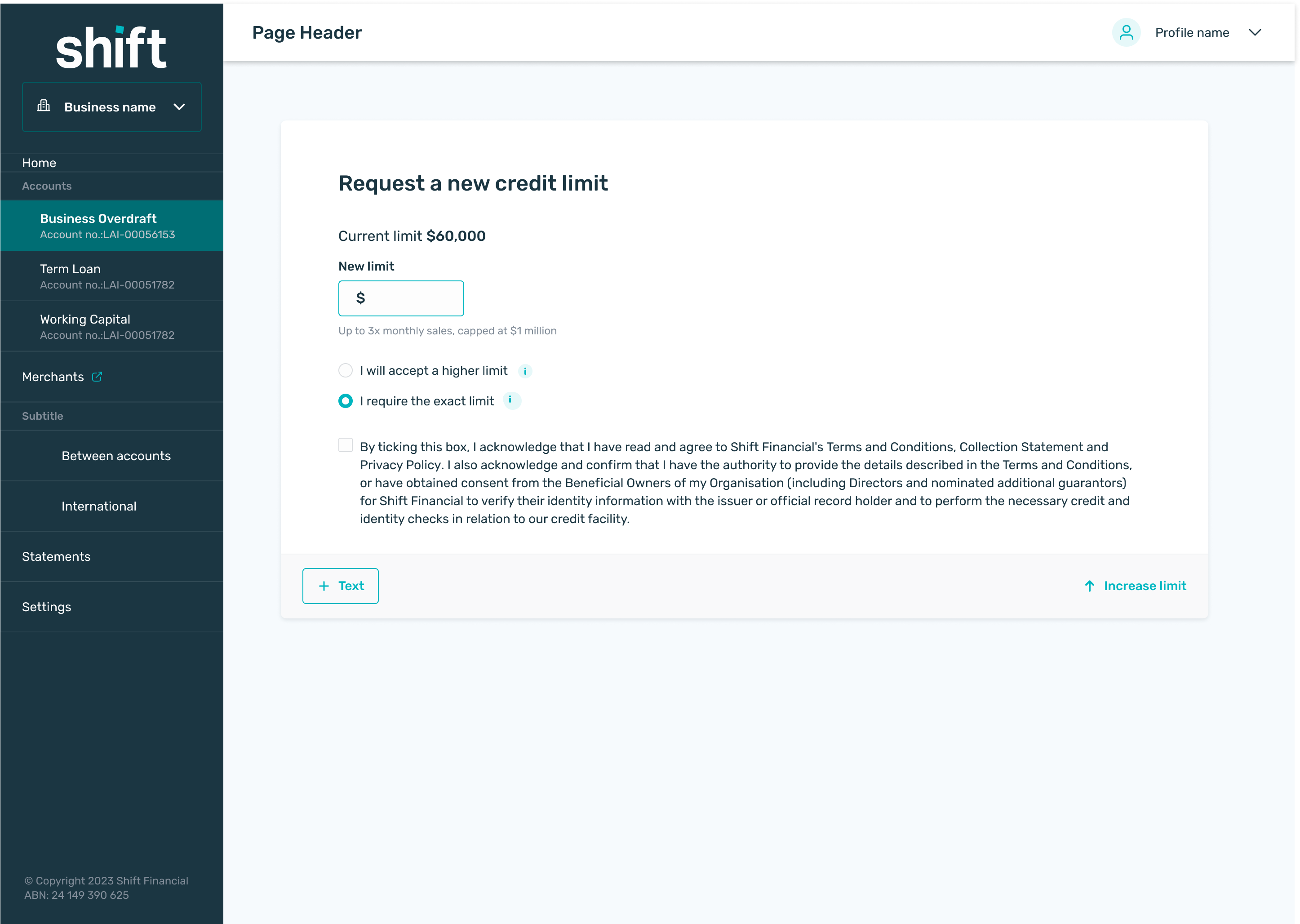

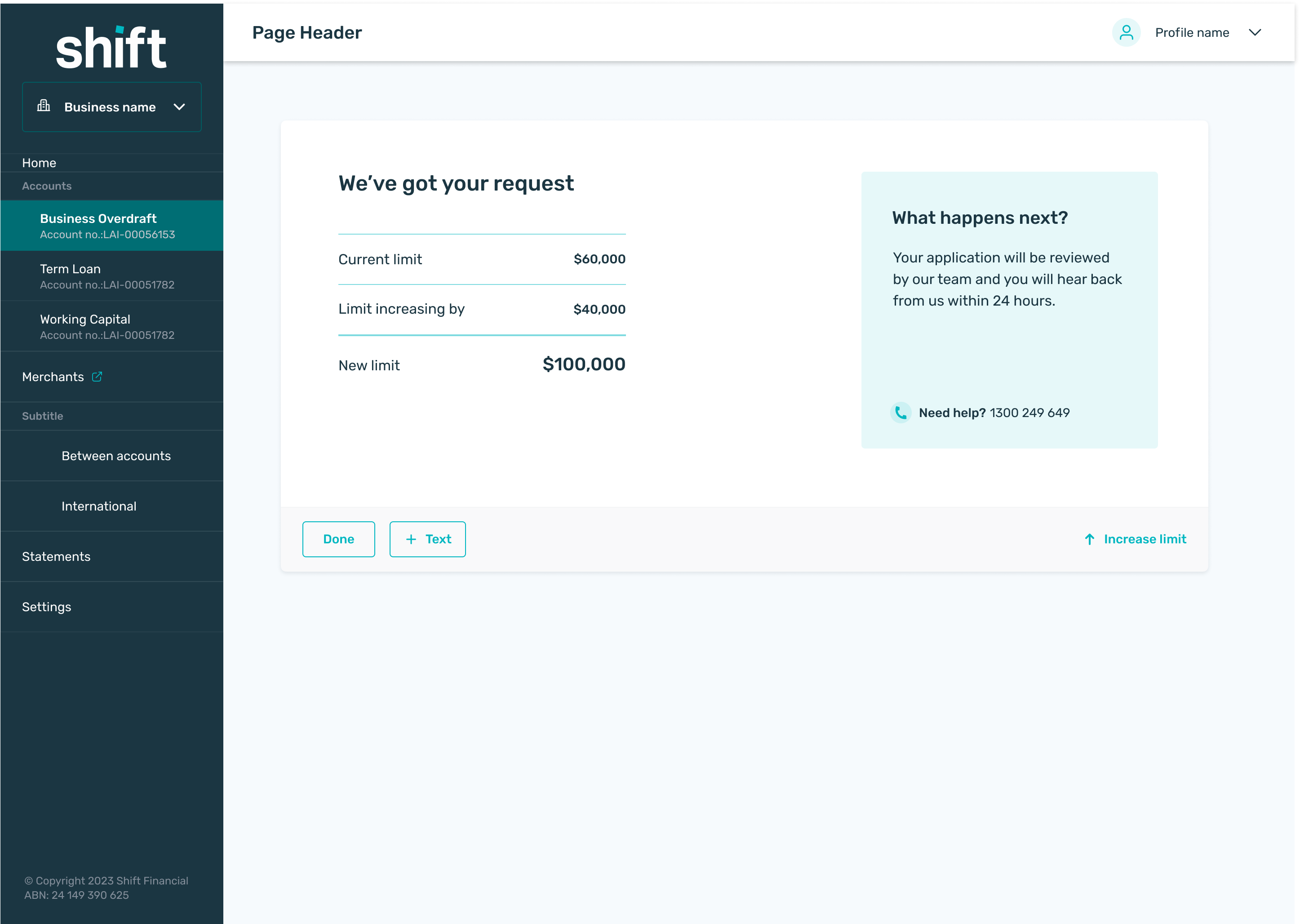

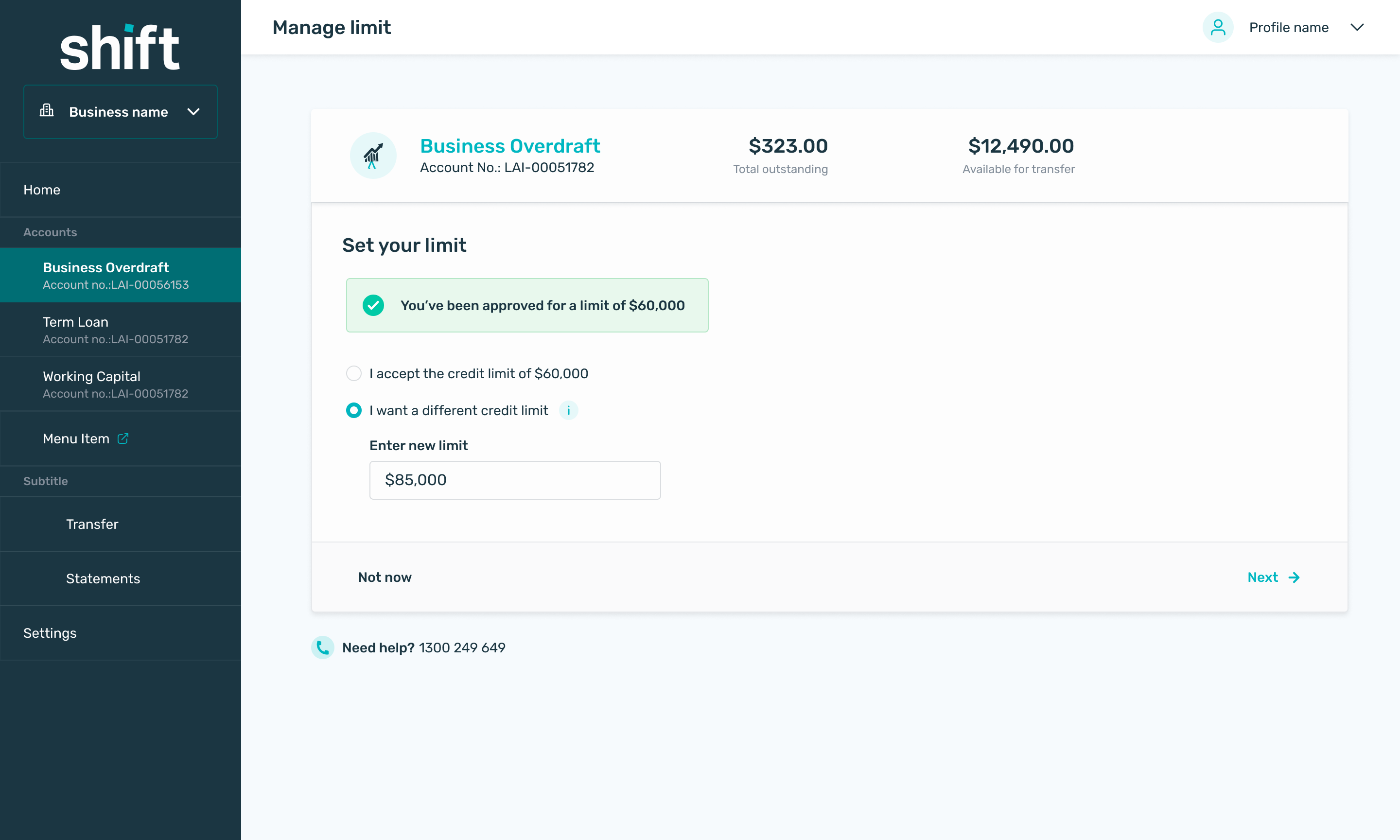

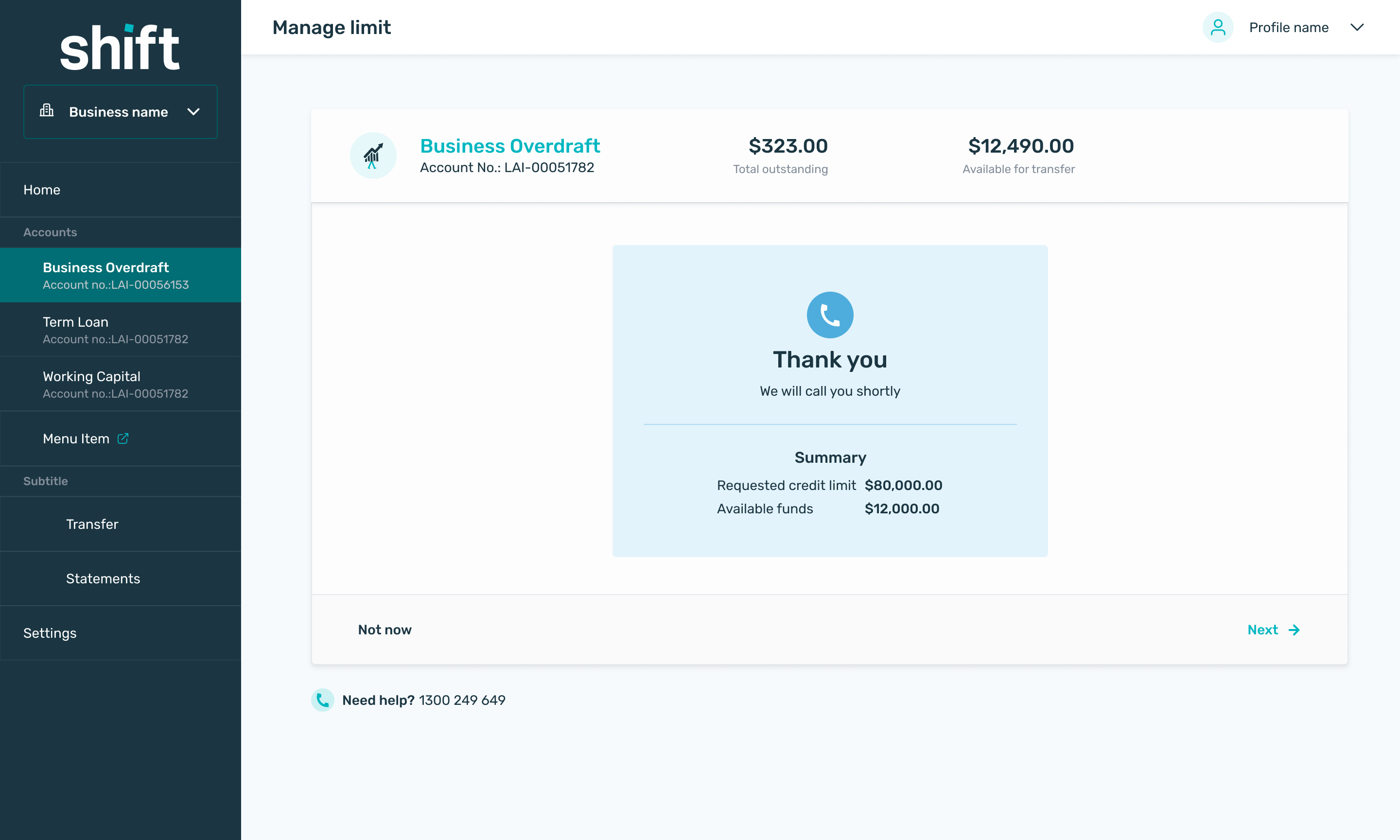

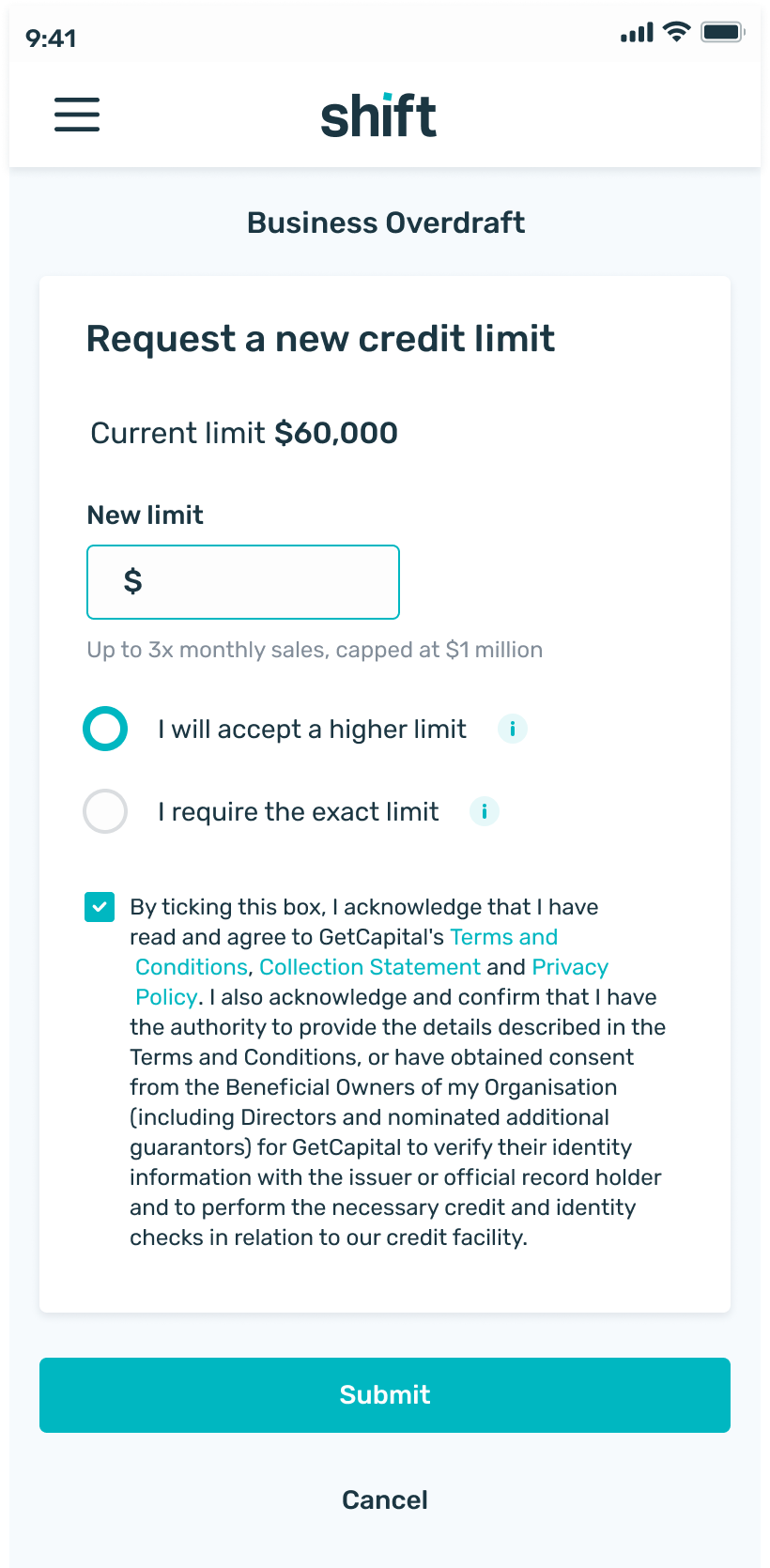

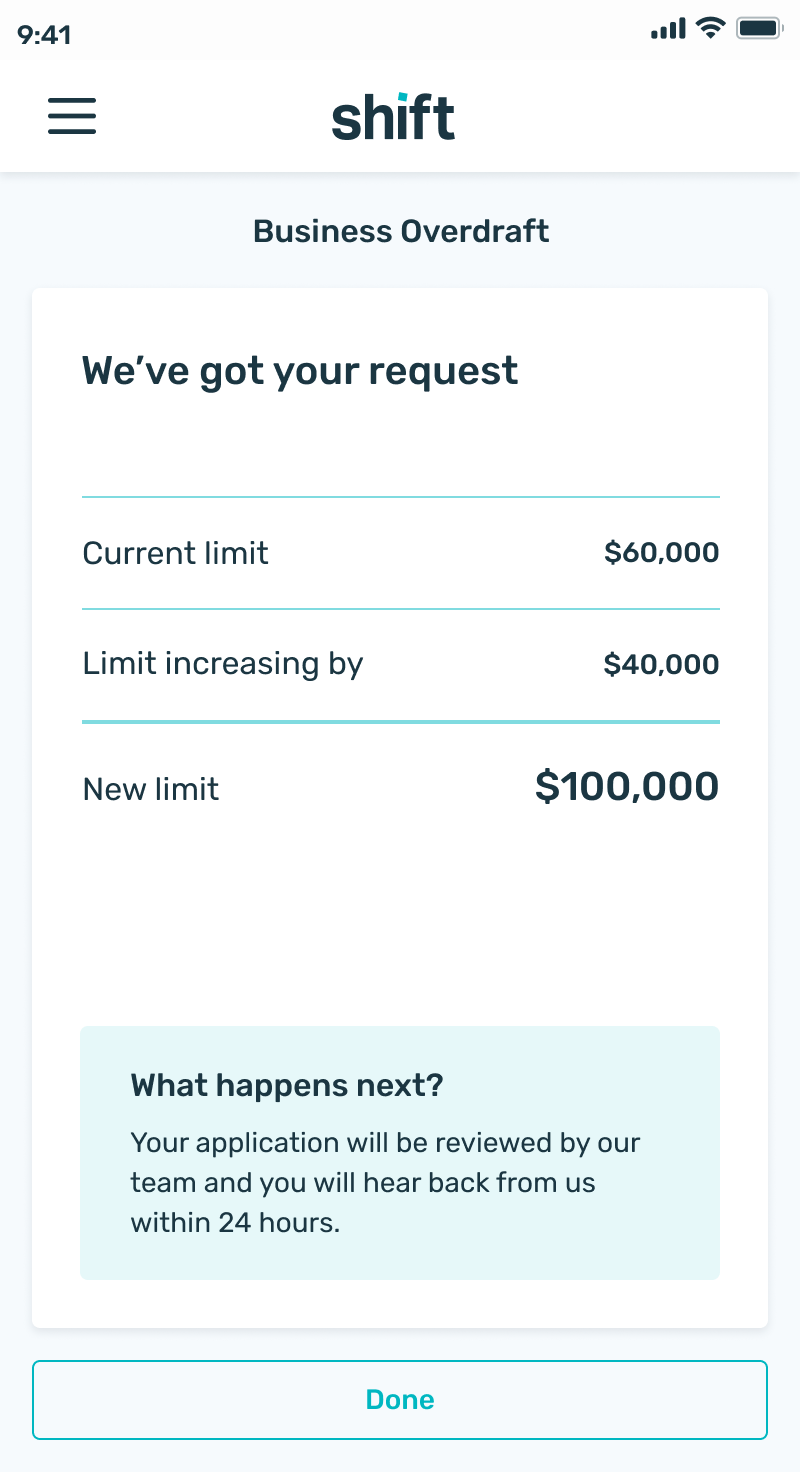

Instant approval for eligible businesses

For businesses that met predefined credit criteria, the system could approve a credit limit increase immediately. These criteria were based on repayment history, current credit utilisation, existing security held by Shift, and internal credit risk scores.

If a business met these requirements, the platform automatically approved the request and applied the new credit limit straight away. This gave trusted customers fast access to additional capital without needing to contact support or wait for manual approval. From a user perspective, the process was simple:

- Enter the desired credit increase

- Confirm the request

- Receive immediate approval and see the updated credit limit in their account

DESIGN

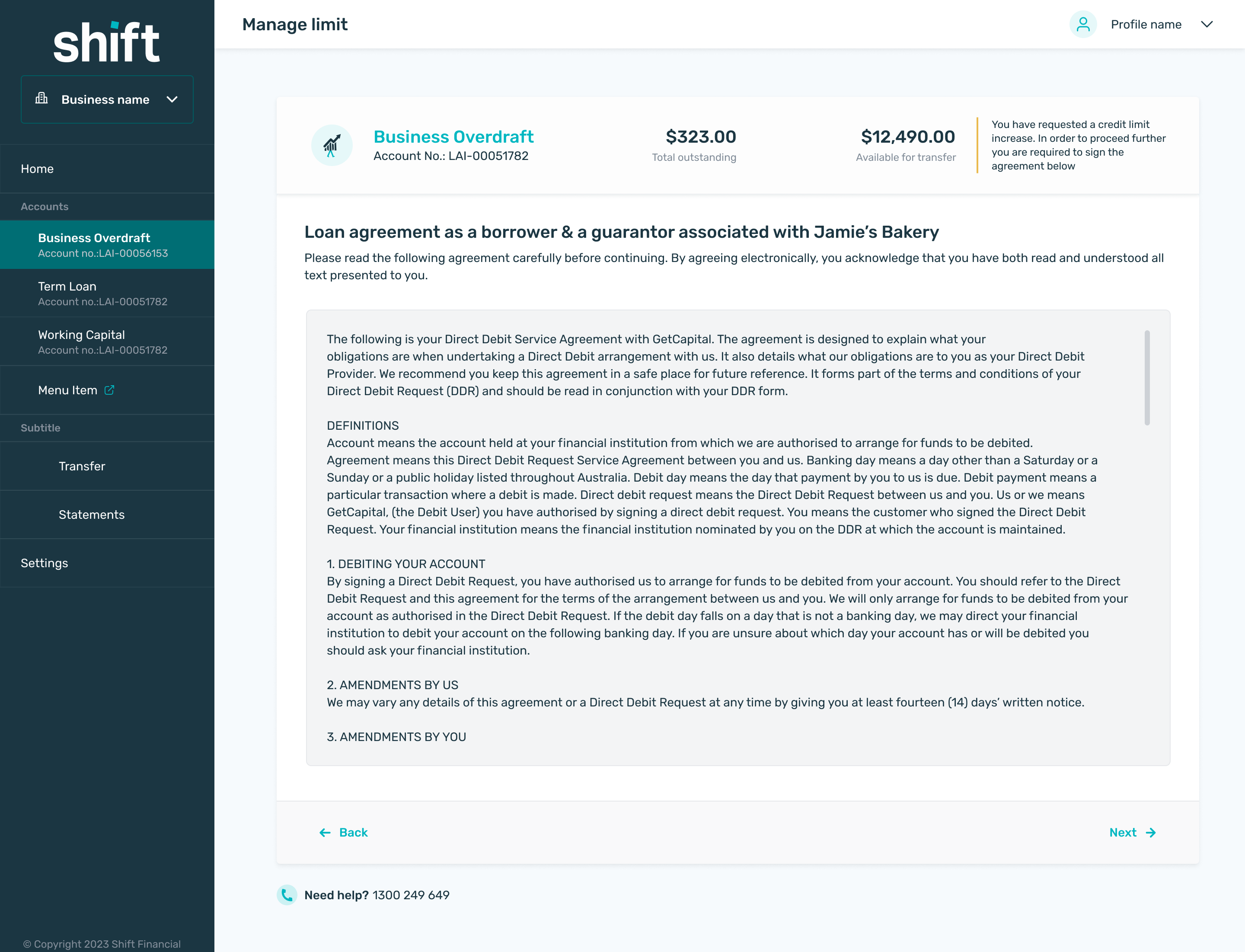

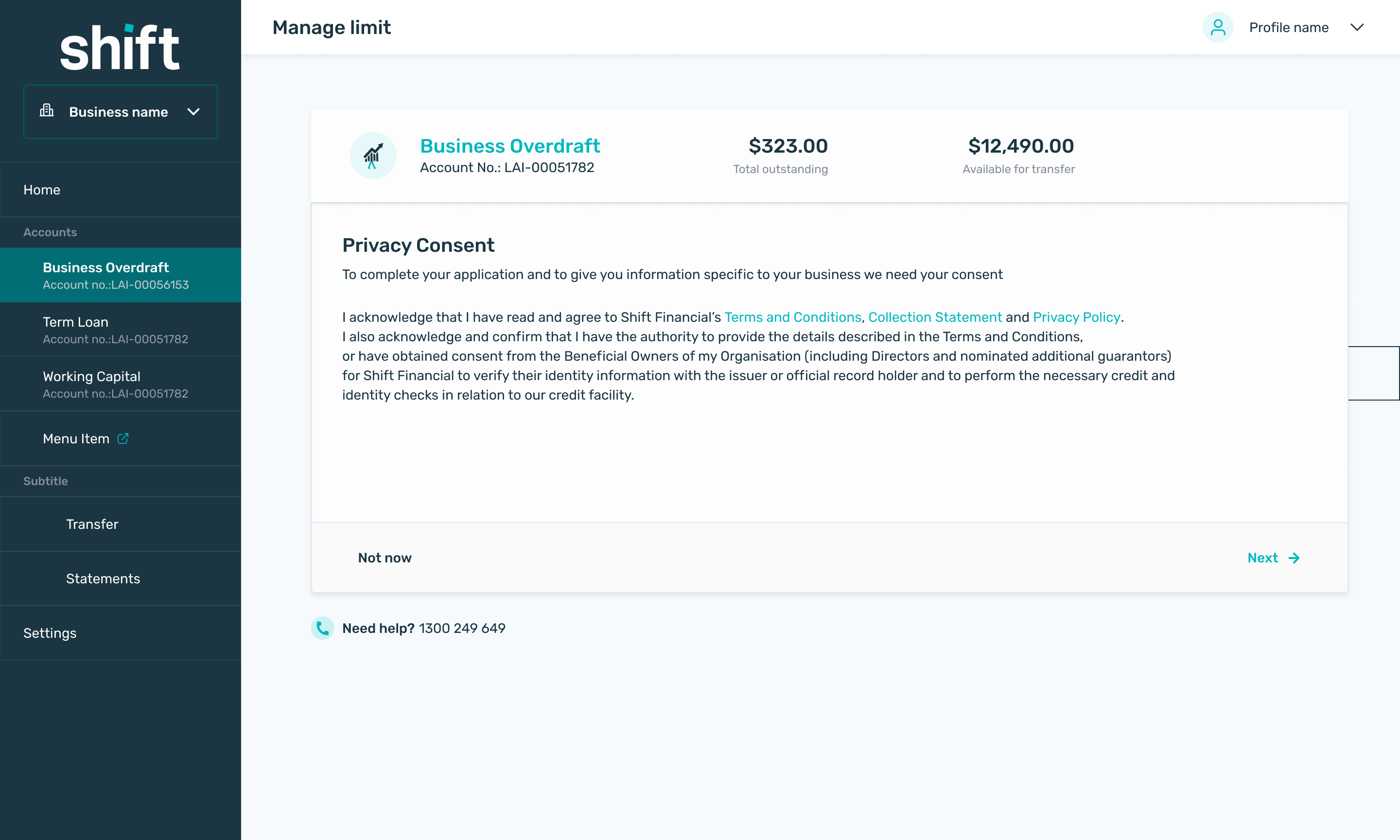

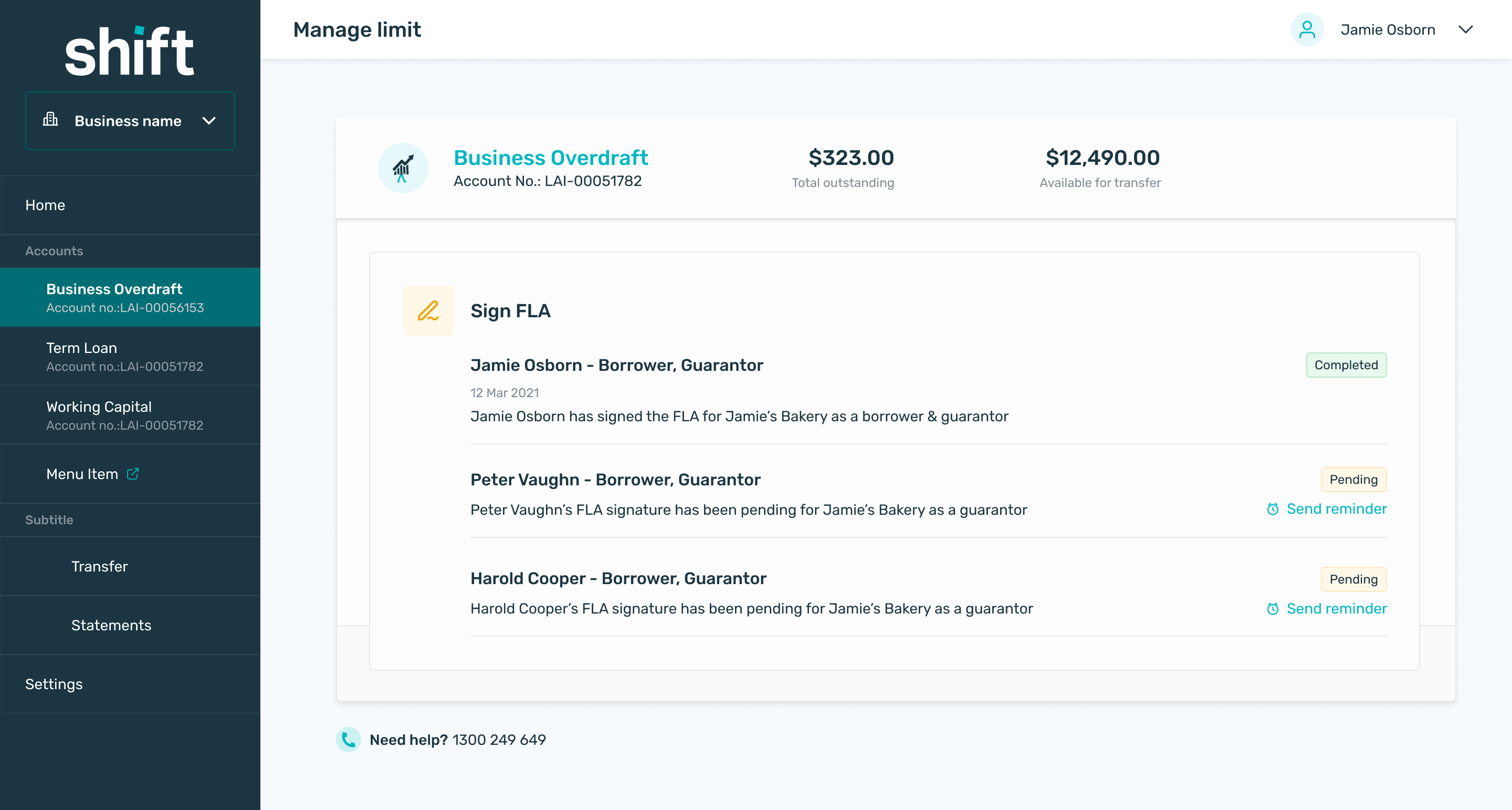

Data collection and FLA signing

For customers on the standard path, the experience involved two steps before a decision could be reached.

Data collection required connecting a bank account via a secure third-party link and uploading financial documents; trust deed and financials. These requirements were fixed by credit policy. What we could control was the experience around them: a step-by-step progress tracker, confirmation when each document was received, and a clear signal that pre-approved customers skip this step entirely.

The Facility Letter of Agreement was the most legally consequential moment in the flow. The design added a plain-English summary alongside the full document - enough context to sign with confidence, without reducing the legal substance.

The 2nd director problem was another edge case. Many of Shift's customers have multiple directors, all of whom must sign the FLA. Once the 1st director signs, the system sends an SMS with a deep-link to the 2nd director. The design provides the 2nd director with full context in a single mobile session. No re-authentication, no re-explaining the situation.

DESIGN

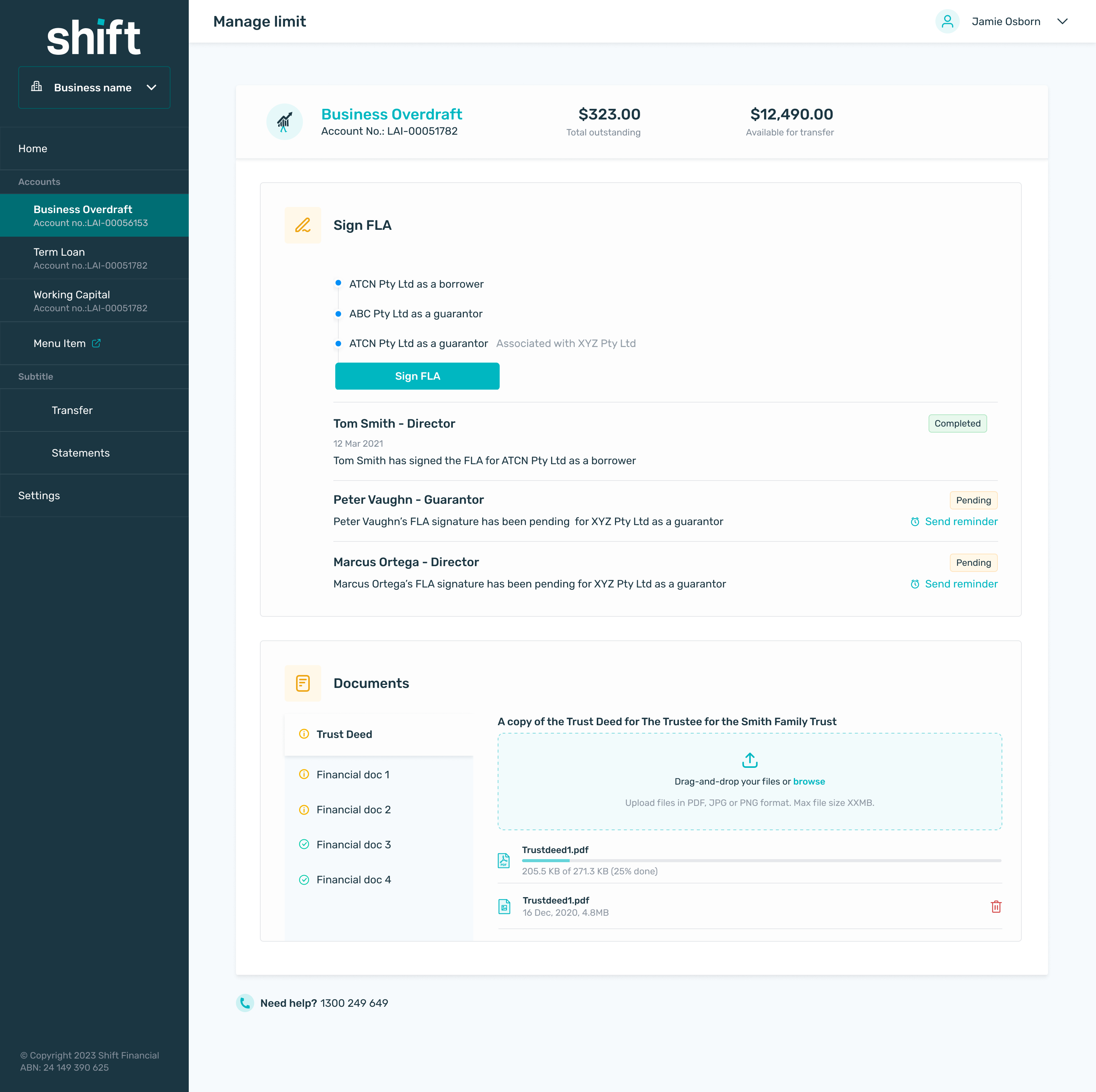

Transparent application tracking for manual approvals

Not every request could be approved automatically. Larger increases, or businesses with more complex financial profiles, still required review from the credit team. For these cases, the focus was on transparency and clarity.

Instead of submitting a request and waiting with no feedback, businesses could now see:

- Confirmation that their request had been submitted

- The current status of their application

- Estimated timelines for review

- Requests for additional documents or information

The design also included simple ways for users to upload required documents or provide extra details, reducing the back-and-forth that previously happened over phone and email.

DESIGN

Redesigning the customer journey

How the experience changes across all nine stages for the customer, 2nd director, and credit team.

The redesigned customer experience journey across all nine stages.

DESIGN

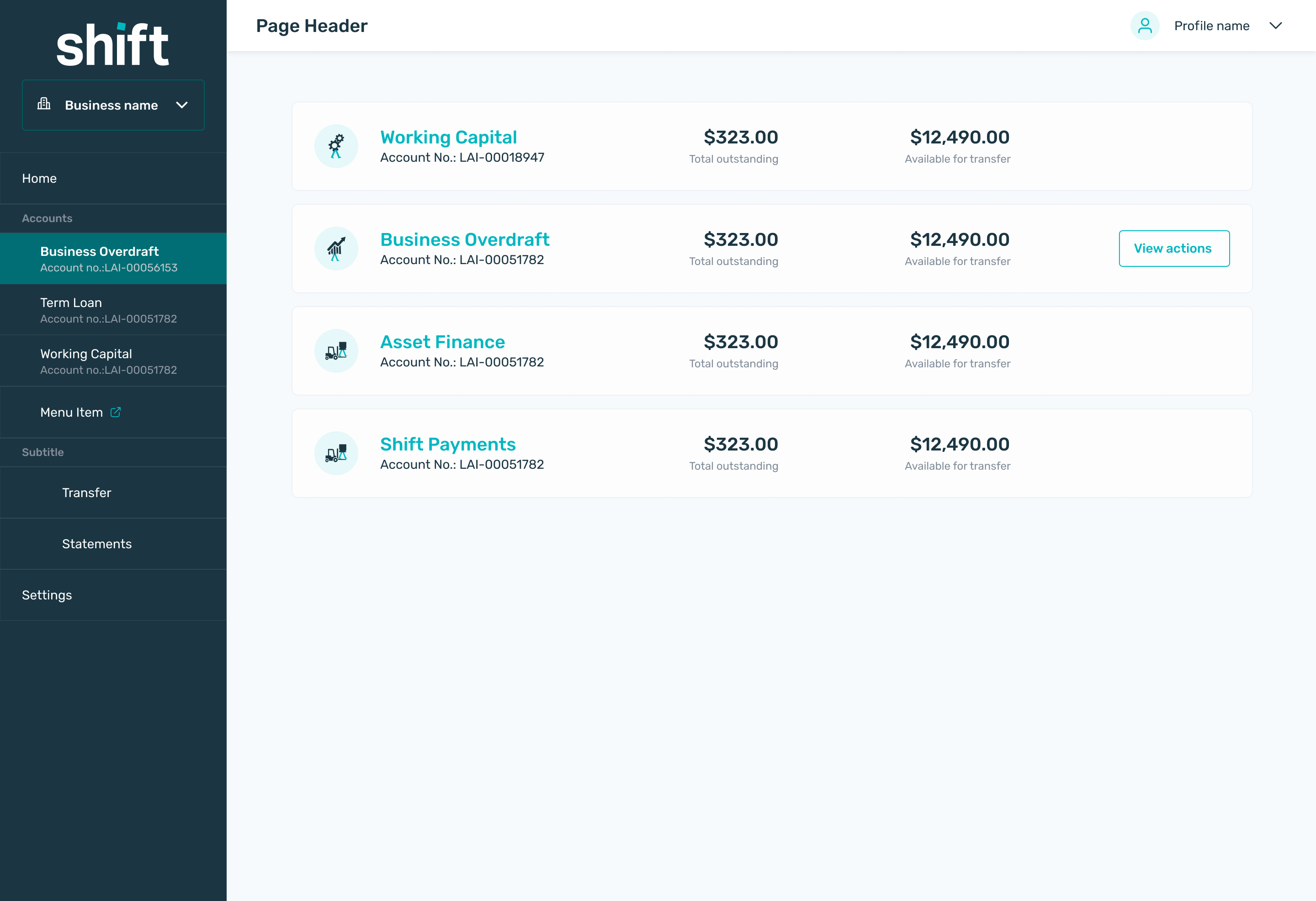

Desktop (auto-approval)

A selection of the desktop auto-approval UI designs

DESIGN

Desktop (manual-approval)

A selection of the desktop manual-approval UI designs

DESIGN

Mobile (auto-approval)

A selection of the mobile auto-approval UI designs

DESIGN

Manual dashboard

Dashboard to manage credit limit increase process for customers who don't meet pre-approval requirements

BEFORE

A manual, phone-based process

- Customer contacts Shift support by phone

- Transferred to the credit team

- Answers questions verbally; documents requested by email

- No confirmation, no tracking, no status visibility

- Approval takes several days

- No explanation if declined

AFTER

A transparent, instant experience

- CLI entry point surfaced on account dashboard

- Pre-approved customers: instant decision, limit updated immediately

- Standard path: structured data collection with progress tracking

- FLA signing: plain-English summary, digital signature, automated 2nd director notification

- Manual review: live application tracker, inline document upload, estimated timelines

- Declined customers: specific reasons and next-step guidance

IMPACT

Turning friction into capital

Within 90 days of launch, $2M in additional business credit had been issued. For pre-approved customers, the time to approval dropped to zero - a request that previously took several days and multiple phone calls was resolved in minutes.

Support call volume for credit limit requests fell significantly as the self-serve route absorbed enquiries that had previously required a human handoff.

Beyond the initial metrics, the feature also established the infrastructure for future improvements. The two-path architecture, instant approval and manual review, gave the credit team a clear framework to refine eligibility criteria over time, expanding the proportion of customers who could be pre-approved as the data set grew. The application tracker and document upload flow gave the operations team visibility they hadn't had before, making the manual review process faster and more consistent even for cases that couldn't be automated.

KEY LEARNINGS

Automation requires cross-team trust

Designing financial automation required deep collaboration with credit and compliance teams to ensure risk was managed appropriately.

KEY LEARNINGS

Transparency builds confidence

Providing application status and clear timelines helped maintain trust even when approvals required manual review.

KEY LEARNINGS

Self-serve unlocks business growth

By removing friction from the credit increase process, the platform enabled customers to access capital faster while helping the business scale.

REFLECTION

Designing within constraints

This project required navigating a set of fixed constraints - regulatory requirements, multi-director sign-off rules, and fragmented backend systems - that couldn't be simplified away. Rather than treating them as blockers, the design process was about finding the right solution within these boundaries.

The FLA plain-English summary, the step-by-step data collection tracker, and the 2nd director signing status all operate entirely within the legal and compliance requirements.

The 2nd director flow remains the main unresolved problem in the journey. An in-platform signing status tracker and a resend option would close the most significant gap in the current experience. I'd also explore proactive CLI nudges, surfacing the entry point when utilisation crosses a defined threshold, before the customer hits their limit rather than after.

Selected Projects

Bolt AppFintech · Mobile app · B2C · Startup

AmaysimTelco · Native app · B2C

ABC · iView appVOD · Native app · B2C

Milestone · pControlFintech · Responsive web · SaaS · B2B

Shift · Edit InstallmentsFintech · Responsive web · B2B

CBA · DisputesBanking · Native app · B2C

Sydney Airport · VIPTravel · Responsive web · B2C

CBA · SDLC NavigatorFintech · Web app · B2B

NickelcloudOperations · SaaS · B2B · Startup

CBA · Transaction Banking PortalFintech · Responsive web · B2B

P&O Cruises · Cruise Booking SiteTravel · Responsive web · B2C

All of UsFintech · Mobile app · B2C · Startup

CBA · System Architecture VisualisationFintech · Responsive web · B2B

DTA · Relationship Authorisation ManagerGovernment · Responsive web · B2B

Standard Chartered · Trade Finance AppFintech · Mobile app · B2B

Advice IntelligenceFintech · SaaS · B2B